Revenues

THE FISCAL REGIME

As per the Belize Petroleum Act, Revised Edition 2000 and the Belize Petroleum Regulations, 1992, the Government enters into Production Sharing Agreements with reputable companies who pass the established screening process with the objective to explore for petroleum resources within Belize.

The current fiscal regime used in Belize is a hybrid of a royalty/tax and production sharing regime with a 10% working interest option for the Government in fields declared commercial.

REVENUES

The Petroleum Act and Schedule 1 of the Petroleum Regulations mandates all petroleum companies who hold licenses to make payment to the Government of Belize, in US Dollars, an annual administration fee and surface rental fees.

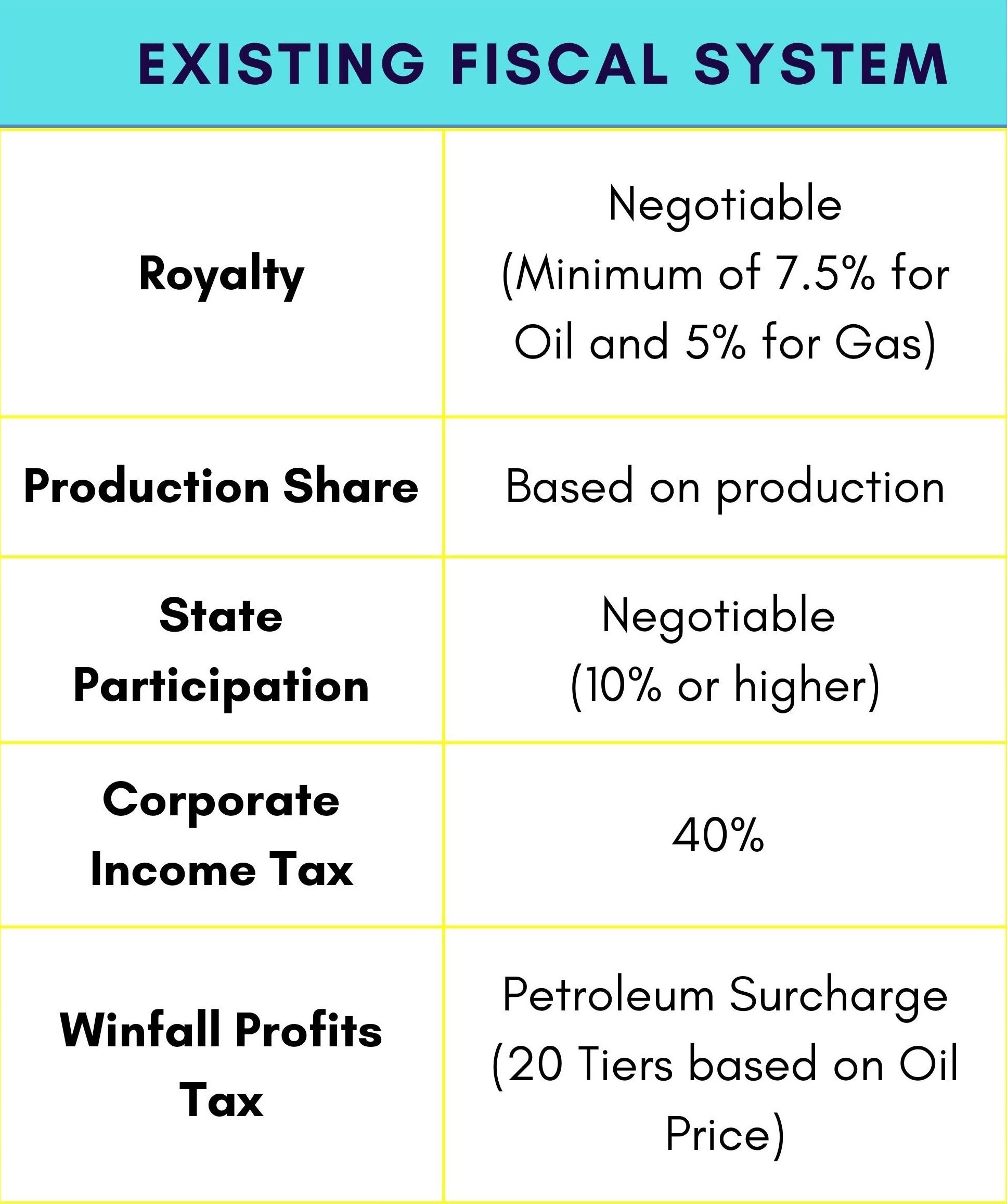

Companies in the production stage pay to the Government of Belize, 5 different forms of revenues from petroleum produced and sold. These fiscal instruments are:

1. Royalty at a minimum of 7.5% on oil and 5% on gas, negotiated in the contract.

2. Government Production Share, negotiated in the contract.

3. Revenues from the Government’s 10% Working Interest in an oilfield.

4. 40% Income Tax.

5. Petroleum Surcharge from windfall profits from high oil prices ($90/bbl for existing field & $100/bbl on new field).

Additionally, producing companies pay a transportation tax per barrel of oil trucked on public highways.